Three rate rises in four months are now hitting household budgets – and many borrowers are reassessing their next move.

Most lenders have already passed on the Reserve Bank’s May cash rate increase to variable-rate borrowers, although some changes are still filtering through.

That means many households are now feeling the combined impact of the February, March and May rate rises all at once.

What the increases mean in dollars

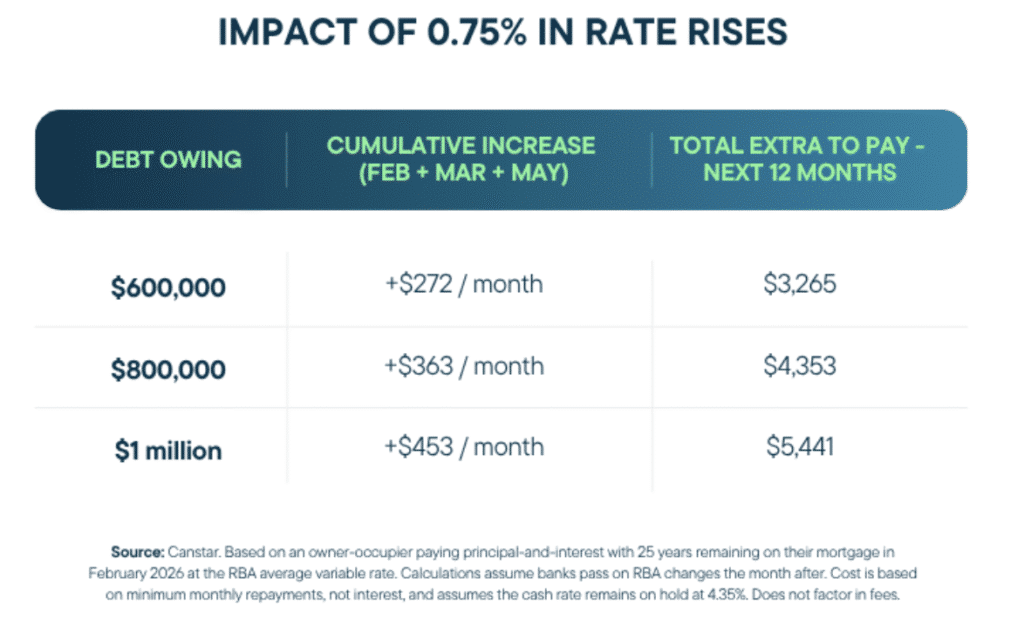

According to Canstar analysis, a borrower with $600,000 remaining on their mortgage is now paying an extra $3,265 per year in repayments following the three increases.

For many households, that’s a meaningful change to monthly cash flow.

How borrowers are responding

Many borrowers are:

-

Reviewing their loan rate and features.

-

Refinancing to more competitive products.

-

Tightening discretionary spending.

-

Building buffers in offset or savings accounts.

Even small adjustments can help improve flexibility if repayments increase further.

Why planning matters

The Reserve Bank has made it clear that inflation remains a concern, and further rate increases are still possible.

That’s why many borrowers are now budgeting for repayments to rise again rather than assuming rates have peaked.

I can help you review your loan, compare what’s available across the market and work through strategies to improve your position in the current environment.

Leave A Comment